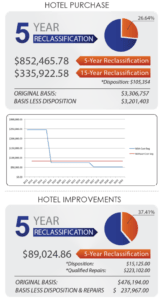

Medical Facility Owners Gain $1,622,280 in Tax Benefits from a Cost Segregation Study

Study Details – Medical Facility Purchase: Engineered Tax Services performed a cost segregation engineering review of building components on a one-story, 15,838 square foot medical office building. The cost segregation benefit included a reclassification of 27.5-year depreciation class life assets into 5 and 15 year class lives, resulting in a combined benefit of $1,622,280 on the