In the realm of real estate investment, savvy investors are always on the lookout for strategies to optimize their portfolios and maximize their returns. One powerful tool often overlooked is the Section 721 Exchange. This mechanism, defined under Section 721 of the Internal Revenue Code, allows an investor to swap properties held for investment or business purposes for shares in a Real Estate Investment Trust (REIT) or an Operating Partnership. Importantly, this transaction does not trigger a taxable event.

This strategy not only offers investors a means to enhance their liquidity but also to diversify their real estate investments. It helps them evade hefty capital gains taxes and depreciation recapture taxes, which can accrue from property sales, thus deferring a significant financial burden.

Understanding the Section 721 Exchange for Real Estate Investment

Many tax professionals and real estate investors are familiar with the 1031 Exchange program. Frequently used by REITs, this program facilitates the acquisition of properties from investors looking to sell their real estate investments. However, in a 1031 Exchange, the investor must find a replacement property to avoid substantial capital gains taxes and depreciation recapture taxes. Additionally, investors often encounter investment restrictions and high costs with REITs.

This is where the Section 721 Exchange shines. It allows investors to sell their real estate investments without having to identify a replacement property. Notably, investors can still obtain these tax benefits even if the real estate has already been sold. They can do so by contributing the sale proceeds to a 721 Operating Company, and in return, they receive Operating Partnership Units.

This transaction, referred to as a 721 Exchange, has several advantages. It's an effective tool for real estate investors seeking tax deferral, estate planning or diversification. However, just like Section 1031, IRC Section 721 is complex, and investors should consult their tax and legal professionals before making any investment decisions.

What Is Section 721 Exchange?

Section 721 exchange allows an investor to swap property held for investment or business purposes for shares in a REIT or an Operating Partnership. These shares can remain in the Operating Partnership or be transferred tax-free to a REIT, should the investor wish to do so.

Operating Partnerships are established to accumulate real estate property and the proceeds from property sales. They can retain the assets or roll them into a REIT if desired. This transaction provides investors with increased liquidity and diversification while deferring capital gains and depreciation recapture taxes that could arise from property sales.

In essence, a Section 721 exchange is an alternative to the 1031 Exchange for investors interested in selling their real estate investments but not keen on finding a replacement property or paying capital gains taxes.

Advantages of the Section 721 Exchange for Tax Deferral and Diversification

In a typical property sale, the seller pays taxes on the capital gains and the depreciation used to defer taxes on the property’s income. The combination of capital gains and depreciation recapture taxes could consume 20-40% of the gains realized from the sale, leaving the investor with less capital for reinvestment. In contrast, a Section 721 Exchange allows investors to defer these taxes and keep their wealth working for them by exchanging their investment property for shares in an Operating Partnership. Key benefits include:

- Diversification: A 721 Exchange empowers an investor to diversify across various aspects, such as geography, industry, tenant and asset class within an Operating Partnership structure. As shareholders in the Operating Partnership, investors engage in a diverse real estate portfolio and aren't solely reliant on one asset for cash flow and appreciation. The Operating Partnership can offer continuous benefits similar to those of real estate ownership, including income, depreciation tax shelter, principal pay-down and appreciation.

- Consistent income: Operating Partnerships can issue dividends or distributions so that the investor has cash flow in amounts similar to when they owned their contributed property.

- Tax deferral: Contributing property or cash from the sale of real estate into the Operating Partnership provides for a deferral of any taxable income from the sale/transfer of the underlying real estate.

- Increased liquidity: Operating Partnerships are established to accumulate real estate property and the proceeds from property sales. They can retain the assets or roll them into a REIT if desired. This transaction provides investors with increased liquidity and diversification while deferring capital gains and depreciation recapture taxes that could arise from property sales.

- Tax safety on sale of a portfolio asset: When an Operating Partnership property is sold, partnership accounting and management fees often generate sufficient expenses to offset any gains investors would be allocated. Risk of gains is usually mitigated by lockout period provisions and indemnification provisions.

- Passive investment: The Section 721 Exchange allows investors to trade an actively managed real estate asset for a portfolio of real estate assets that are actively managed by the principals of an Operating Partnership. This structure allows individual investors to access and rely upon expertise provided by institutional asset management firms for all decisions regarding the real estate portfolio.

- Estate planning: The 721 Exchange is often utilized as an estate planning tool to prepare an investor’s real estate assets to be passed down to heirs. When direct real estate assets are passed to heirs, they are often difficult to quickly liquidate and equally divide among heirs. The 721 Exchange provides a tailored solution that allows the estate to be prepared for easy transfer while deferring the capital gains taxes that have built up over the years.

- Flexibility: For an investor to contribute property to a REIT through an UPREIT transaction, the property must meet the REIT’s stringent investment criteria. However, some well-designed Operating Partnerships can structure the Operating Partnership to attract a larger number of like-minded investors. By utilizing a Section 721 Exchange, an investor can exchange a property that doesn't meet the Operating Partnership's criteria for a fractional interest in a high-quality property or portfolio.

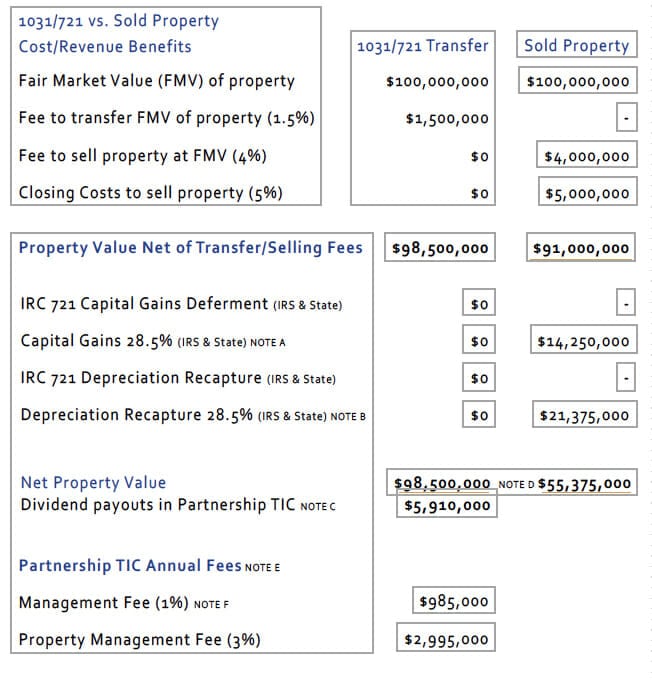

721 Benefits Example

GENERAL NOTE: The noted calculations are for illustrative purposes. The fees stay constant, the values will change for each property. NOTE A: For the purposes of this comparison, we assume a Capital Gain of $50,000,000 or 50% of FMV NOTE B: For the purposes of this comparison, we will assume a Depreciation Recapture of $75,000,000 or 75% of FMV NOTE C: Each property in the TIC will have its own Revenue Stream. For the purposes of this property we use 5% annually NOTE D: The owner of the sold property will find another property which will incur fees, expenses and revenue stream. NOTE E: All fees are tax deductible to the owners of the Partnership TIC NOTE F: This fee is used for our outside Legal, CPA and Tax Preparation (TIC & Personal Reporting)

Conclusion

Section 721 Exchange, an often overlooked yet potent tool in the real estate investment landscape, provides unique benefits to investors such as tax deferral, diversification, steady income, enhanced liquidity and streamlined estate planning. An appealing alternative to a 1031 Exchange, it allows for direct contribution of property or sale proceeds to an Operating Partnership, bypassing the burden of identifying a replacement property and high REIT-associated costs.

However, given its complexity, investors are advised to seek professional tax and legal advice before embarking on this venture. As the real estate market and tax laws continue to change, the Section 721 Exchange remains an effective strategy for savvy investors seeking to optimize their portfolio and navigate the evolving terrain.