In 2017 the Tax Cuts and Jobs Act (TCJA) included significant tax breaks for taxpayers but often when a bill like this is passed, the question is asked “How will we pay for it?”. And one answer was to implement an amortization rule for all research & development (R&D) costs beginning in January of 2022 (five years down the road at that point).

Before 2022 R&D costs were eligible for immediate expensing, and if the R&D tax credit was claimed, those expenses would be added back to prevent double-dipping which took the credit amount from a gross 14% tax credit for eligible expenses to a net tax credit average of 5%-7%.

However, now the TCJA requires all costs relating to R&D must be amortized over 5 years if based in the U.S., or 15 years if they are international costs.

What falls under the definition of R&D costs?

IRS tax code section 174 defines R&D (aka research and experimentation) expenditures as costs incident to the development or improvement of a product. Including patent costs, patent-related attorney’s fees, laboratory costs, salaries, and wages for trial and error, up to the elimination of uncertainty phase.

Products are defined as any pilot model, process, formula, invention, technique, patent, or similar property whether used in the taxpayer’s business or for outside sale or license, as well as amounts paid to outside contracts or consultants for the above activities.

Industries claiming R&D include manufacturing, architectural design, inventors, pharmaceutical companies, medical devices, software companies, businesses building internal use software, and many more.

The R&D tax credit remains permanent

There has been confusion about changes to the R&D tax credit, however, the R&D credit definition and amounts have not changed. The R&D credit itself was made permanent years ago and remains an incentive for taxpayers to invest in U.S.-based innovation and technological advancements in the hard sciences, which include manufacturing, engineering, biology, and computer science.

R&D credits have helped fund billions of dollars of U.S.-based products since its enactment in 1981. In 2012 over $11.6 billion of credits were reported of which 69% went to salaries and wages, 15% to supplies, and 16% to contract research (U.S. Dept of Treasury Tax Analysis October 12, 2016).

Credit has proven to be both a direct and indirect societal benefit to increase U.S. production, patents, innovation, and technological advancements within the U.S.

Tax Implications of Amortization

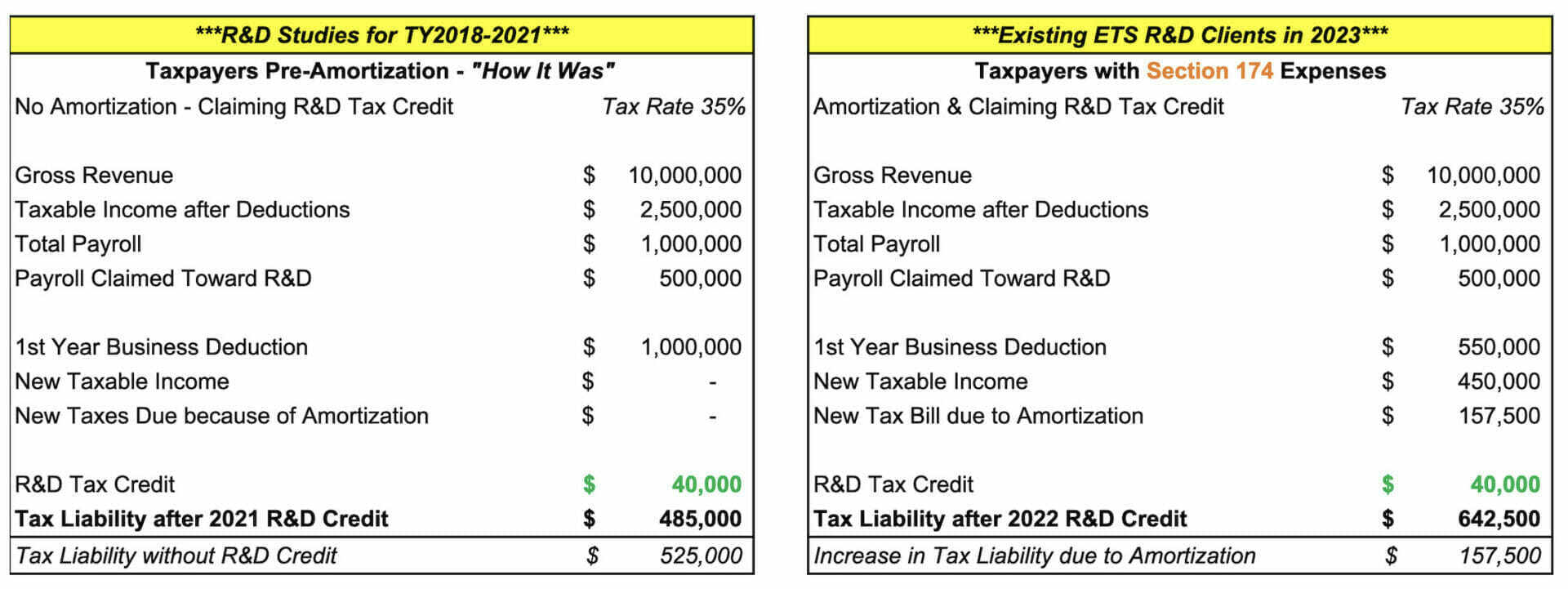

However, this amortization bill now penalizes taxpayers with qualified activity. To see these implications we must look at Taxpayers who have claimed R&D in the past, and those who have not. Below is an example of a taxpayer who claimed R&D credits in 2021 and deducted their eligible costs, and the same scenario with amortized costs in 2022. The amortization rule results in a first-year increase in tax due for 2022, but keep in mind that amortized costs will stack each year until year 5 when annualized costs will be similar to pre-amortization years.

The examples above reflect the increase in a tax liability of $157,500 for a taxpayer amortizing qualified costs as compared to the previous year.

The question then arises if taxpayers should avoid the R&D tax credit altogether, or if those claiming credits historically should elect out of the credit and identification of qualified costs. For taxpayers who have claimed R&D historically, they have set a precedent of having qualified activity and a change in the allocation of these costs could increase IRS scrutiny of current and future expenses, or previous credit claims in which costs were attributed to research.

For taxpayers who have not claimed R&D credits historically, the credit can provide significant value to help fund qualified costs and innovation. Avoiding the tax credit is leaving money on the table that would be lost if not claimed in the first 3 years. But claiming it will increase tax liability for the first four to five years, which is the unintended impact of this amortization bill and directly disincentivizes taxpayers to invest in research activities.

It is recommended to review these rules in depth with your tax professional to understand the pros and cons. And keep in mind that if, or when, the amortization rule is changed then it will be back to business as usual!

Future Outlook

There has been industry consensus that a delay to the amortization rule would be passed in late 2022 before it was implemented, and the subsequent change of accounting filed. However, this extension was removed from the appropriation bill passed in December 2022. It is hoped that the first quarter of 2023 will include an additional budget bill to delay this through 2026 but it does not have bipartisan support and its outlook is unclear.

We suggest you reach out to your local elected officials to encourage their support in a delay of the amortization rule.

If you have additional questions regarding R&D credits or this amortization rule please reach out to Engineered Tax Services.