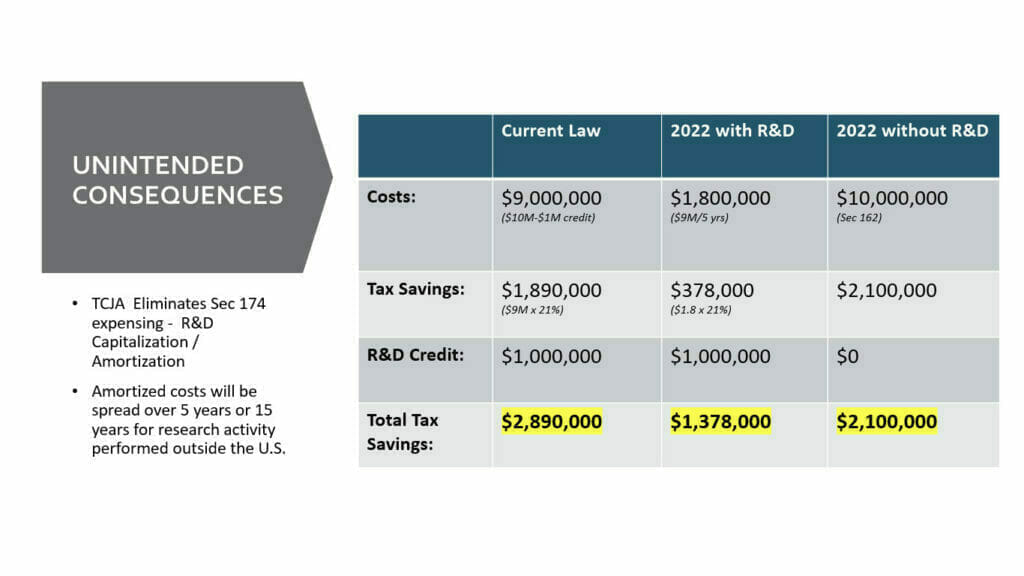

The End of Immediate Expensing?

The outcome of this legislative tussle is by no means certain. We may well witness a delay on this amortization rule, since pending drafts of the Build Back Better Act have included the delayed application of amortization until 2026.

If amortization becomes the law, what recourse is there for taxpayers? There are five strategies taxpayers should be marshalling now to counteract for this possibility:

- Cash flow planning

Optimizing cash flow tax planning can offset a potential tax burden. In this case, federal and state loss carryforwards may be helpful. Please note that federal loss carryforwards may be subject to 80% taxable limitations. Taxpayers with loss carryforwards in California may benefit from Assembly Bill 85; for taxpayers with taxable income of more than $1 million, net operating losses are suspended.

- FASB ASC Topic 740

Under FASB ASC Topic 740, businesses are required to analyze and disclose income tax risk, so their income tax expense for financial reporting are recognized according to U.S. generally accepted accounting principles (GAAP).

Accounting for income tax under ASC 740 affects how a taxpayer capitalizes R&D costs, regarding:

- Deferred tax assets

- Cash taxes

- Effective tax rate

- The bottom line when assessing new White House tax proposals

- Documenting R&D tax credits

Nothing nullifies a taxpayer’s chances of obtaining R&D tax credits more than insufficient documentation. Meticulously detailed supporting documentation is a non-negotiable! Ascertain that the level of detail in your documentation meets IRS standards. It can also be smart for taxpayers to review their R&D tax credits to ensure they can capture the greatest dollar amount.

- Accounting methods

Savvy taxpayers may also want to consider adopting alternative accounting methods, such as by accelerating deductions or deferring revenue, for instance. By changing their accounting method, if a taxpayer has been employing an inadmissible method of accounting, they can correct it by deferring the correction’s cost over four years, while protecting against prior-year audit adjustments subject to interest and penalties. As a rule, accounting method changes should be considered part of a taxpayer’s overall cash flow strategy.

Technical accounting for R&D cost centers and accounting policies can identify costs that could be recategorized as other general and administrative costs.

Be Prepared

Will the amortization rule will become a reality next year? Only a soothsayer would know, but in the meantime, being forewarned means becoming prepared!